Risk capital

Risk capital represents the amounts of money (capital) that are allocated to high-risk venues (e.g., speculative activity, high-risk, high-reward investments). In other words, it refers to the funds designated for investments that carry a great amount of risk, with the potential for high returns. Generally speaking, risk capital denotes financial resources (that is, own funds requirements, equity, shareholder funds) that are provided by the owners / investors of a company as a means to support its business and operations. By its specific nature, risk capital is void of any explicit guarantee that those funds will be returned (and hence the funds are said to be at-risk).

However, and in general contexts, all types of monetary and non-monetary assets that are exposed to potential losses in value are classified as risk capital. This includes any money or assets that are exposed to a possible loss in value, in addition those funds earmarked for highly speculative investments. Risk capital relates to the equity financing of companies that have perceived high-growth potential during their early set-up and growth stages.

In a regulatory context, risk capital is essential that a bank maintains a sufficient buffer, or risk capital, to cover potential losses. Shareholders have an interest in making high returns on the capital invested in the bank and thus that part of shareholders’ equity is usually assigned to account for losses that may arise in the process.

Capital at risk

Capital at risk (CaR) is a measure of risk that reflects the probability that the return of initial capital (principal) invested would be doubtful up to a certain degree. If the performance of an investment lies within specified limits, repayment of initial capital invested can be made as per contractual terms. Otherwise, the provider of the capital (invested amount) could lose some or all of the initial capital invested. Generally speaking, capital at risk is defined as the amount of capital that is set aside by an individual or entity as a means by which certain types of risk can be covered.

In the specific context of credit risk, capital at risk (CaR) is measured as a function of the probability distribution of economic loss. The probability distribution of economic loss is, in turn, a function of the distributions and correlations of certain factors: potential replacement cost, default and recovery.

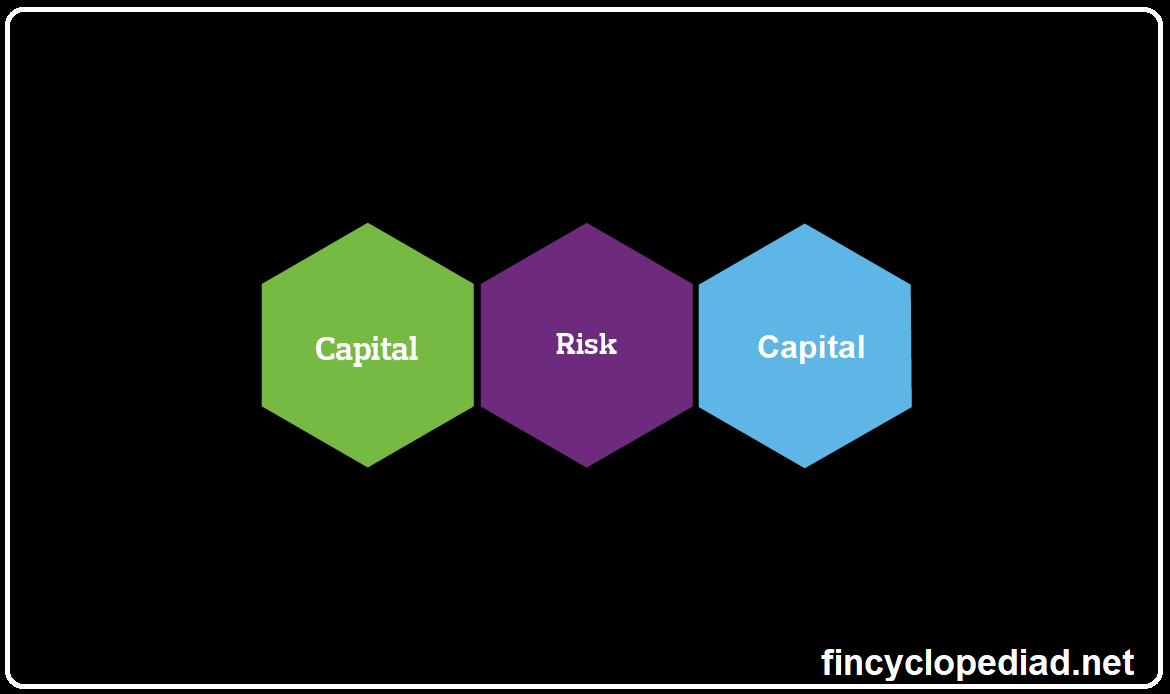

Capital at risk should not be confused with capital risk or risk capital. Capital risk represents the risk arising from the partial or total investment amount that is invested and is exposed to risk of loss. For example, if an individual has initially invested $5,000 in stocks. This initial investment is the capital invested or paid in. Therefore, the capital risk here is $5,000, irrespective of the current market value of these stocks at a certain point in time (that might be greater or smaller than the original capital invested.

Risk capital, on the other hand, refers to amounts of money allocated to high-risk venues (e.g., speculative activity, high-risk, high-reward investments). However, and in general contexts, all types of monetary and non-monetary assets that are exposed to potential losses in value are classified as risk capital.